Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

June 9, 2026 3:24 PM

Every finance team lives with some version of this tension. Lock down spending too tightly, and you slow the business; employees can't buy what they need when they need it, and every purchase becomes a negotiation. Give people too much freedom and costs balloon, policy compliance drops, and month-end close turns into an archaeology project.

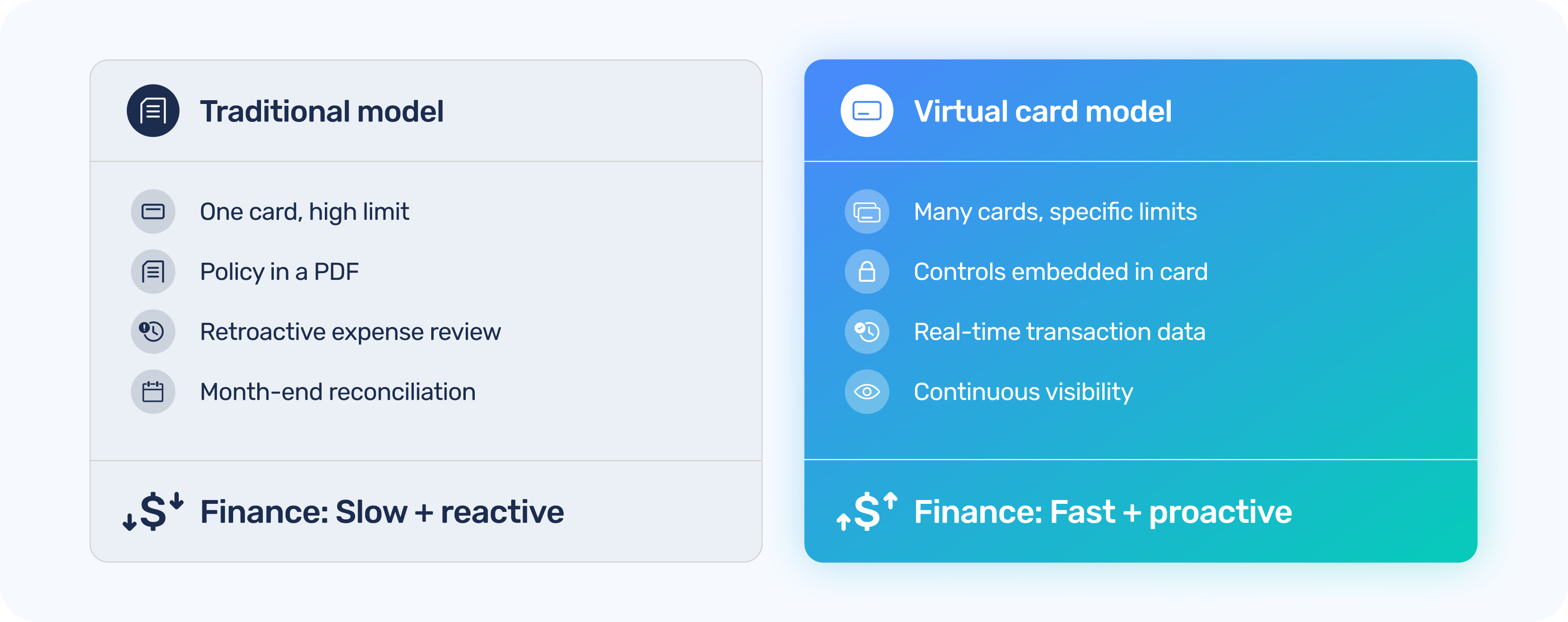

Most finance teams try to solve this with policies. The policies do not stick. The real fix is structural: designing payment systems where the control is built into the instrument, not enforced after the fact by a human being reviewing expense reports.

The instinct when facing a spending problem is to restrict. Put everything above $50 through an approval workflow. Require three quotes for any purchase over $500. Add a layer of sign-off for any new vendor. These controls feel rigorous, but they have real costs: they slow decision-making, they create approval backlogs, and they train employees to route around the system for small purchases that should not require oversight.

The deeper problem is that blanket restrictions treat all spending as equally risky, which it is not. A $400 flight for a sales rep is not the same risk profile as a $400 charge from a vendor that finance has never seen before. Smart controls need to be sensitive to context, not just dollar amounts.

The virtual card model flips the control architecture. Instead of one single physical card with a large limit and a policy document that governs how it is used, you issue many virtual cards from that one physical card with small, specific limits that are appropriate for their intended purpose. An employee traveling to a conference gets a card valid for the trip dates, limited to the conference hotel and reasonable meal spend. A team ordering supplies gets a card locked to the approved vendor with a budget equal to the order.

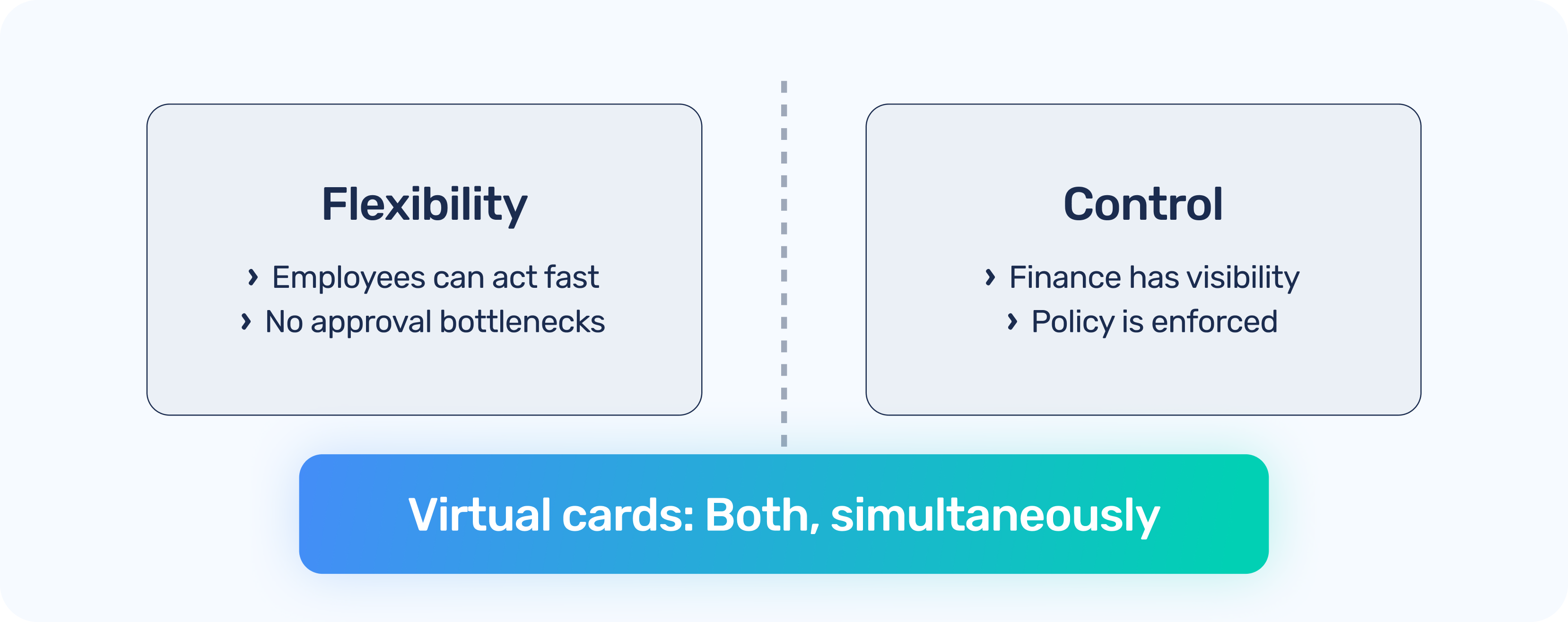

In this model, the employee has genuine flexibility; they can make decisions and act without waiting for approval, and finance has genuine control; the limit is structural, not behavioral. The employee can't accidentally overspend because the card stops working at the limit. Finance does not have to review every transaction because the transaction already conforms to what was authorized.

One reason finance teams default to pre-approval for spending is the visibility gap: if you cannot see what employees are spending until they submit an expense report, you need to approve things in advance because that is your only control point. Real-time visibility changes this calculus entirely.

When every transaction is visible to finance the moment it posts, with context about who spent it, on what, and against which budget, the approval workflow becomes optional for most transactions. Finance can review in near real time. Anomalies surface immediately rather than at the end of the month. Employees can act without waiting for sign-off on routine purchases.

This is the operating model that high-functioning finance teams are moving toward. Not more approvals, but better visibility. Not less flexibility, but smarter constraints. At Extend, this is exactly what we have built: purpose-specific virtual cards with real-time transaction feeds, so finance teams can give employees the autonomy the business needs while maintaining the oversight finance requires. Talk to us about how Extend makes this work in practice!

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Every finance team lives with some version of this tension. Lock down spending too tightly, and you slow the business; employees can't buy what they need when they need it, and every purchase becomes a negotiation. Give people too much freedom and costs balloon, policy compliance drops, and month-end close turns into an archaeology project.

Most finance teams try to solve this with policies. The policies do not stick. The real fix is structural: designing payment systems where the control is built into the instrument, not enforced after the fact by a human being reviewing expense reports.

The instinct when facing a spending problem is to restrict. Put everything above $50 through an approval workflow. Require three quotes for any purchase over $500. Add a layer of sign-off for any new vendor. These controls feel rigorous, but they have real costs: they slow decision-making, they create approval backlogs, and they train employees to route around the system for small purchases that should not require oversight.

The deeper problem is that blanket restrictions treat all spending as equally risky, which it is not. A $400 flight for a sales rep is not the same risk profile as a $400 charge from a vendor that finance has never seen before. Smart controls need to be sensitive to context, not just dollar amounts.

The virtual card model flips the control architecture. Instead of one single physical card with a large limit and a policy document that governs how it is used, you issue many virtual cards from that one physical card with small, specific limits that are appropriate for their intended purpose. An employee traveling to a conference gets a card valid for the trip dates, limited to the conference hotel and reasonable meal spend. A team ordering supplies gets a card locked to the approved vendor with a budget equal to the order.

In this model, the employee has genuine flexibility; they can make decisions and act without waiting for approval, and finance has genuine control; the limit is structural, not behavioral. The employee can't accidentally overspend because the card stops working at the limit. Finance does not have to review every transaction because the transaction already conforms to what was authorized.

One reason finance teams default to pre-approval for spending is the visibility gap: if you cannot see what employees are spending until they submit an expense report, you need to approve things in advance because that is your only control point. Real-time visibility changes this calculus entirely.

When every transaction is visible to finance the moment it posts, with context about who spent it, on what, and against which budget, the approval workflow becomes optional for most transactions. Finance can review in near real time. Anomalies surface immediately rather than at the end of the month. Employees can act without waiting for sign-off on routine purchases.

This is the operating model that high-functioning finance teams are moving toward. Not more approvals, but better visibility. Not less flexibility, but smarter constraints. At Extend, this is exactly what we have built: purpose-specific virtual cards with real-time transaction feeds, so finance teams can give employees the autonomy the business needs while maintaining the oversight finance requires. Talk to us about how Extend makes this work in practice!

Every finance team lives with some version of this tension. Lock down spending too tightly, and you slow the business; employees can't buy what they need when they need it, and every purchase becomes a negotiation. Give people too much freedom and costs balloon, policy compliance drops, and month-end close turns into an archaeology project.

Most finance teams try to solve this with policies. The policies do not stick. The real fix is structural: designing payment systems where the control is built into the instrument, not enforced after the fact by a human being reviewing expense reports.

The instinct when facing a spending problem is to restrict. Put everything above $50 through an approval workflow. Require three quotes for any purchase over $500. Add a layer of sign-off for any new vendor. These controls feel rigorous, but they have real costs: they slow decision-making, they create approval backlogs, and they train employees to route around the system for small purchases that should not require oversight.

The deeper problem is that blanket restrictions treat all spending as equally risky, which it is not. A $400 flight for a sales rep is not the same risk profile as a $400 charge from a vendor that finance has never seen before. Smart controls need to be sensitive to context, not just dollar amounts.

The virtual card model flips the control architecture. Instead of one single physical card with a large limit and a policy document that governs how it is used, you issue many virtual cards from that one physical card with small, specific limits that are appropriate for their intended purpose. An employee traveling to a conference gets a card valid for the trip dates, limited to the conference hotel and reasonable meal spend. A team ordering supplies gets a card locked to the approved vendor with a budget equal to the order.

In this model, the employee has genuine flexibility; they can make decisions and act without waiting for approval, and finance has genuine control; the limit is structural, not behavioral. The employee can't accidentally overspend because the card stops working at the limit. Finance does not have to review every transaction because the transaction already conforms to what was authorized.

One reason finance teams default to pre-approval for spending is the visibility gap: if you cannot see what employees are spending until they submit an expense report, you need to approve things in advance because that is your only control point. Real-time visibility changes this calculus entirely.

When every transaction is visible to finance the moment it posts, with context about who spent it, on what, and against which budget, the approval workflow becomes optional for most transactions. Finance can review in near real time. Anomalies surface immediately rather than at the end of the month. Employees can act without waiting for sign-off on routine purchases.

This is the operating model that high-functioning finance teams are moving toward. Not more approvals, but better visibility. Not less flexibility, but smarter constraints. At Extend, this is exactly what we have built: purpose-specific virtual cards with real-time transaction feeds, so finance teams can give employees the autonomy the business needs while maintaining the oversight finance requires. Talk to us about how Extend makes this work in practice!

Every finance team lives with some version of this tension. Lock down spending too tightly, and you slow the business; employees can't buy what they need when they need it, and every purchase becomes a negotiation. Give people too much freedom and costs balloon, policy compliance drops, and month-end close turns into an archaeology project.

Most finance teams try to solve this with policies. The policies do not stick. The real fix is structural: designing payment systems where the control is built into the instrument, not enforced after the fact by a human being reviewing expense reports.

The instinct when facing a spending problem is to restrict. Put everything above $50 through an approval workflow. Require three quotes for any purchase over $500. Add a layer of sign-off for any new vendor. These controls feel rigorous, but they have real costs: they slow decision-making, they create approval backlogs, and they train employees to route around the system for small purchases that should not require oversight.

The deeper problem is that blanket restrictions treat all spending as equally risky, which it is not. A $400 flight for a sales rep is not the same risk profile as a $400 charge from a vendor that finance has never seen before. Smart controls need to be sensitive to context, not just dollar amounts.

The virtual card model flips the control architecture. Instead of one single physical card with a large limit and a policy document that governs how it is used, you issue many virtual cards from that one physical card with small, specific limits that are appropriate for their intended purpose. An employee traveling to a conference gets a card valid for the trip dates, limited to the conference hotel and reasonable meal spend. A team ordering supplies gets a card locked to the approved vendor with a budget equal to the order.

In this model, the employee has genuine flexibility; they can make decisions and act without waiting for approval, and finance has genuine control; the limit is structural, not behavioral. The employee can't accidentally overspend because the card stops working at the limit. Finance does not have to review every transaction because the transaction already conforms to what was authorized.

One reason finance teams default to pre-approval for spending is the visibility gap: if you cannot see what employees are spending until they submit an expense report, you need to approve things in advance because that is your only control point. Real-time visibility changes this calculus entirely.

When every transaction is visible to finance the moment it posts, with context about who spent it, on what, and against which budget, the approval workflow becomes optional for most transactions. Finance can review in near real time. Anomalies surface immediately rather than at the end of the month. Employees can act without waiting for sign-off on routine purchases.

This is the operating model that high-functioning finance teams are moving toward. Not more approvals, but better visibility. Not less flexibility, but smarter constraints. At Extend, this is exactly what we have built: purpose-specific virtual cards with real-time transaction feeds, so finance teams can give employees the autonomy the business needs while maintaining the oversight finance requires. Talk to us about how Extend makes this work in practice!

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)